It happened again. I blinked, and my daughters have somehow grown and matured beyond the mental picture I had in my head. Of course, it didn't really happen overnight. I noted the ever-taller marks on the measuring board and changing interests. Still, it shocked me as the incremental changes, none drastic enough to be noteworthy, have accumulated to produce two beautiful young ladies much bigger than the little girls I'm accustomed to.

These under-the-radar progressions happen in our world more frequently than we realize, and a prime example is the maturation that has occurred in the landscape of corporate ownership.

Several decades ago, the private equity industry was a niche part of the American economy that had minimal relevance on a larger scale. But through slow and steady growth, it has become an influential part of the economy with profound implications for investors, especially as the investable opportunities in publicly traded companies continues to dwindle.

The Shrinking Public Market

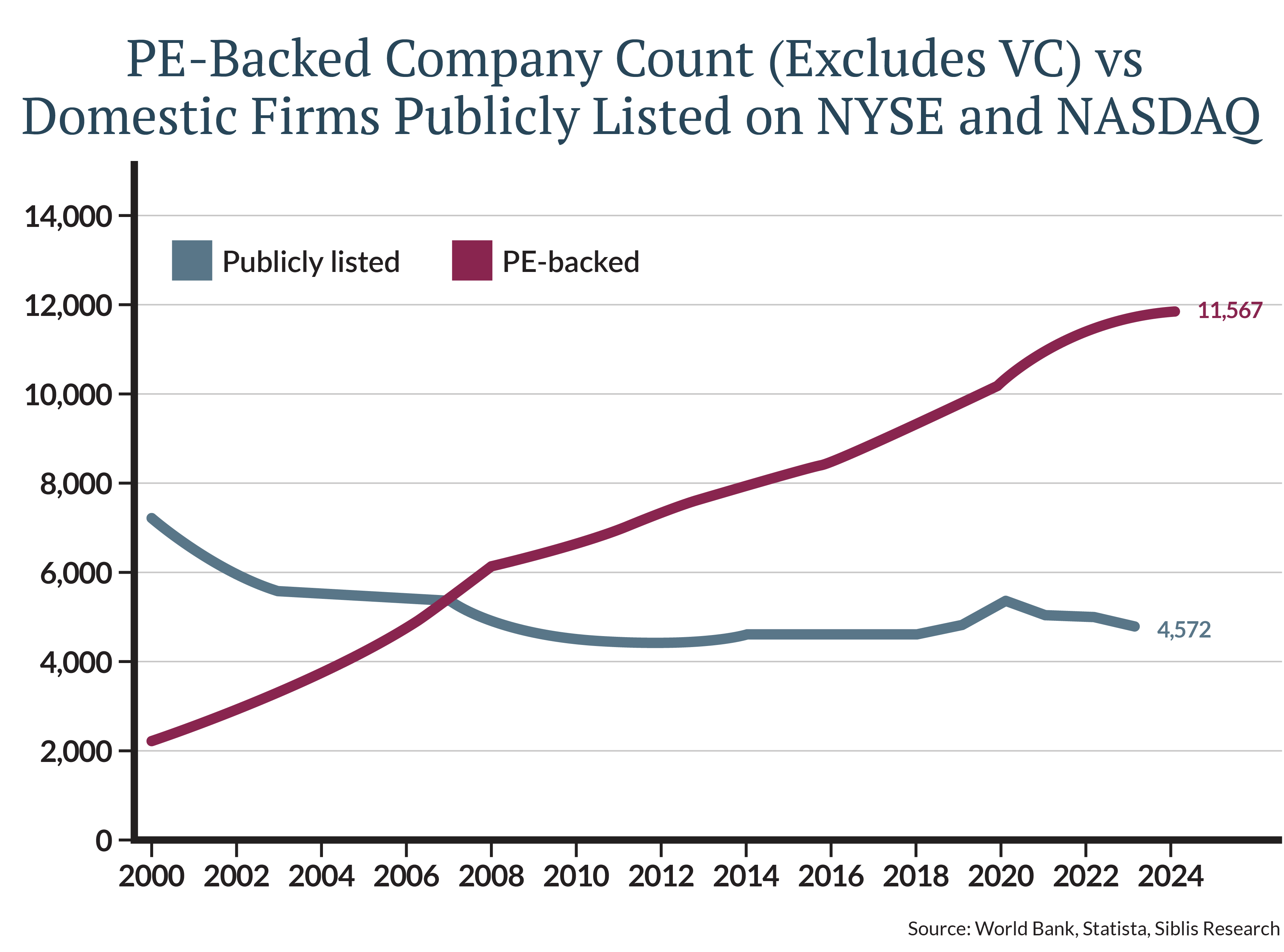

In the 2000s, the U.S. stock market comprised nearly 8,000 publicly traded companies. Today, that number has dropped to roughly 4,500. [Figure 1] This shift is indicative of a structural change driven by the growing attractiveness of private capital, and private equity (PE) firms have played a significant role. In the past decade, PE firms have raised capital, at first small and now vast amounts, enabling them to invest, manage, and grow companies while avoiding public listings.

Why Companies Are Staying Private Longer

There are several motivations for business owners and investors to choose to remain private longer rather than go public:

- Access to capital: The public markets were traditionally the only avenue to raise significant capital to fund expansion and growth. But, the modern financial landscape has changed. Private funding, such as private equity and venture capital, have become increasingly accessible, offering companies the capital they need without the regulatory burdens and scrutiny of public markets.

- Regulatory environment: In the aftermath of financial crises during the early and mid-2000s, the regulatory requirements for public companies became increasingly onerous, particularly since the passage of the Sarbanes-Oxley Act in 2002. Public companies face a heavy burden of compliance costs and ongoing disclosure obligations, which a recent Bank of America report estimated can cost a public company $8-$11 million annually. In contrast, private companies have more flexibility and less regulatory overhead.

- Control and flexibility: Staying private allows management teams to maintain greater control over business strategy. Public market investors commonly evaluate businesses against quarterly performance metrics. This short-term view can come at the expense of long-term results. Private companies, particularly under private equity ownership, have the freedom to implement long-term growth strategies, pursue acquisitions, or restructure operations without the pressure of quarterly earnings expectations.

Implications for Investors

The shift toward private ownership presents both challenges and opportunities for investors.

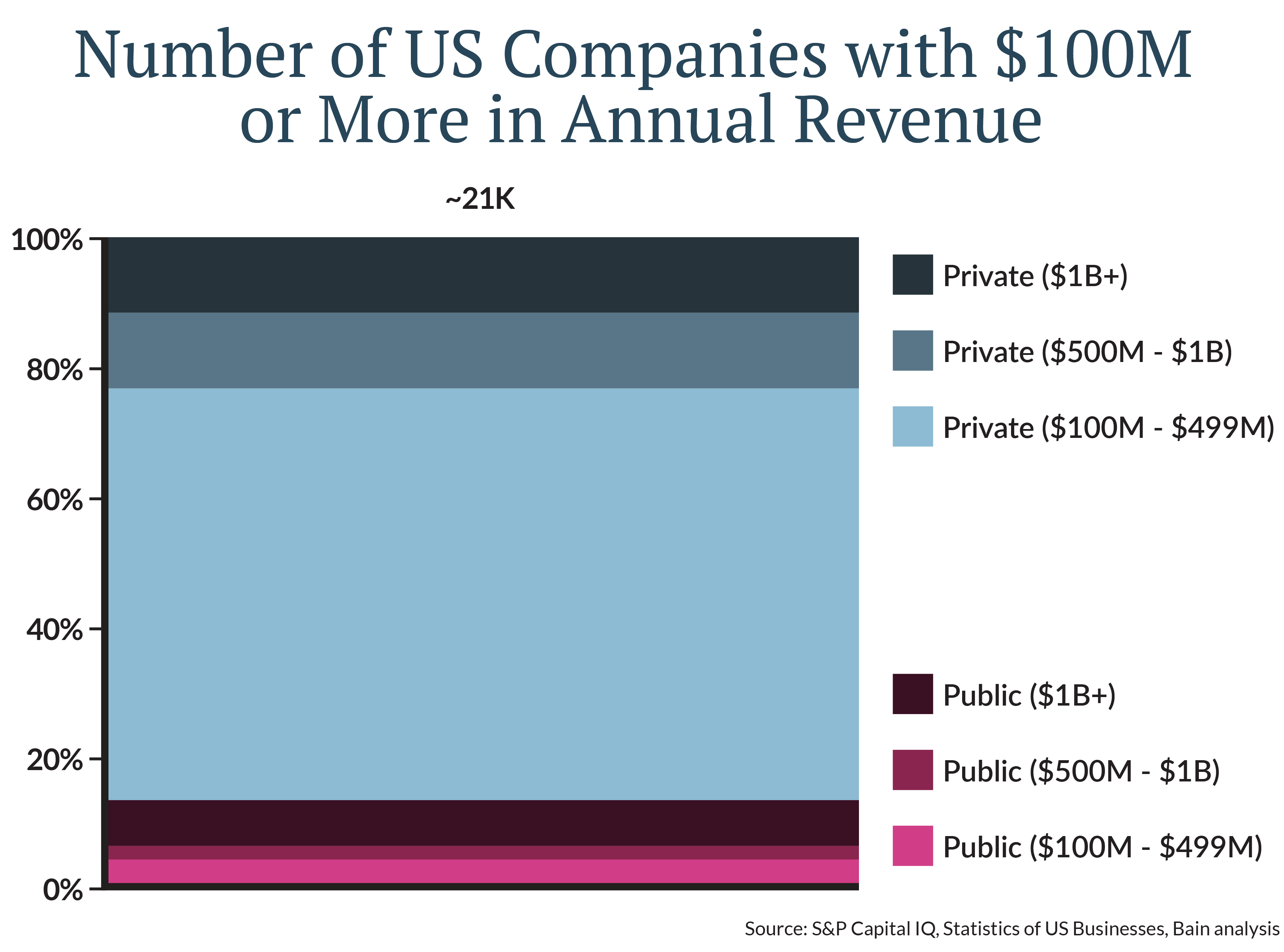

- Narrower opportunity set: Investors limited to investment in publicly traded businesses are exposed to a narrow and shrinking portion of the total economy. As reflected in the chart below [Figure 2], more than 80% of American companies with revenue greater than $100 million are privately owned.

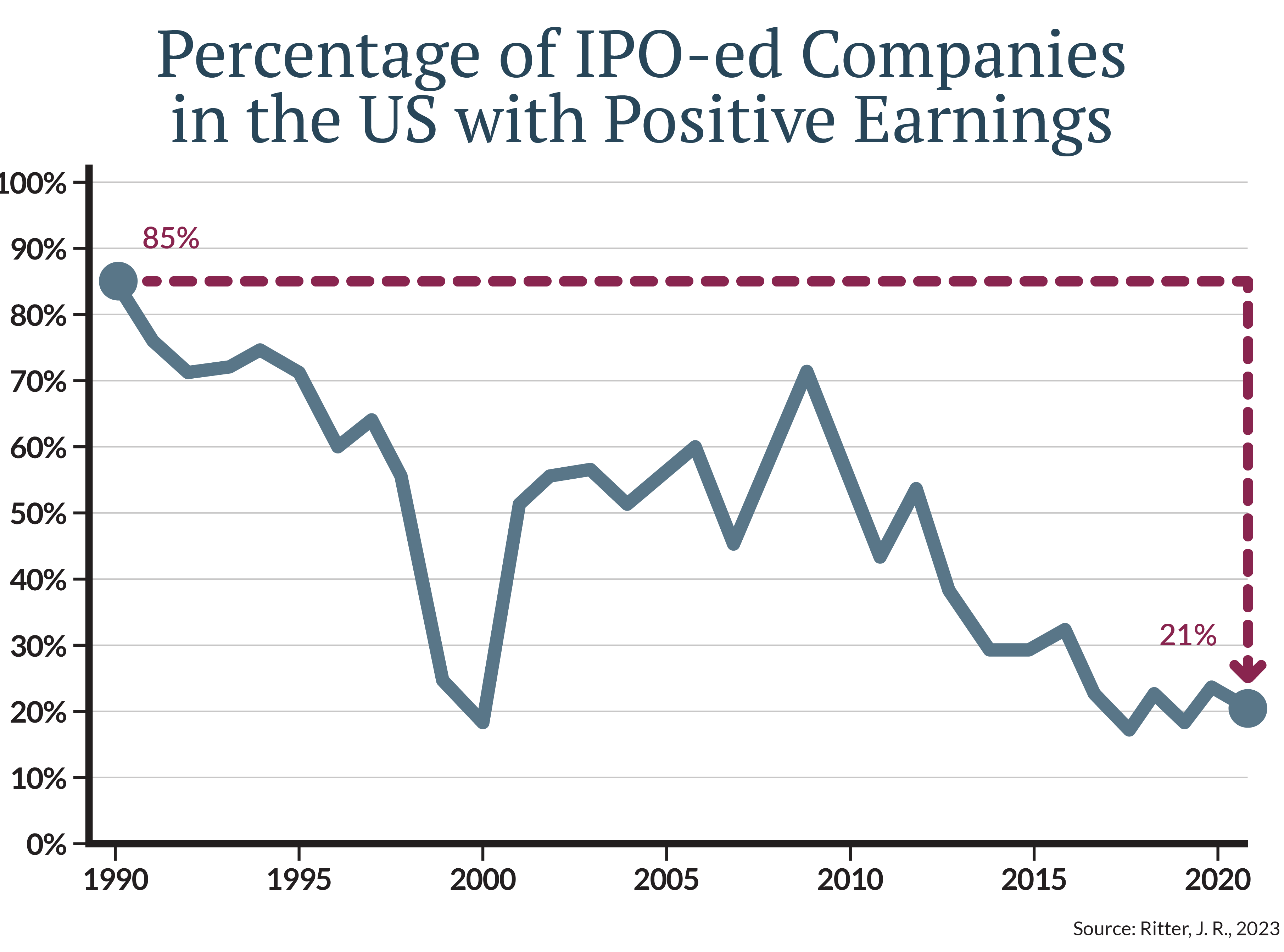

- Declining quality: Going public once represented a graduation to the "next level," a sign that a business had come of age. That is no longer the case, as today's IPOs are frequently unproven businesses raising money to fund big ideas with uncertain outcomes. This is highlighted by the persistent decline in the percentage of IPOs with positive earnings, as shown. [Figure 3]

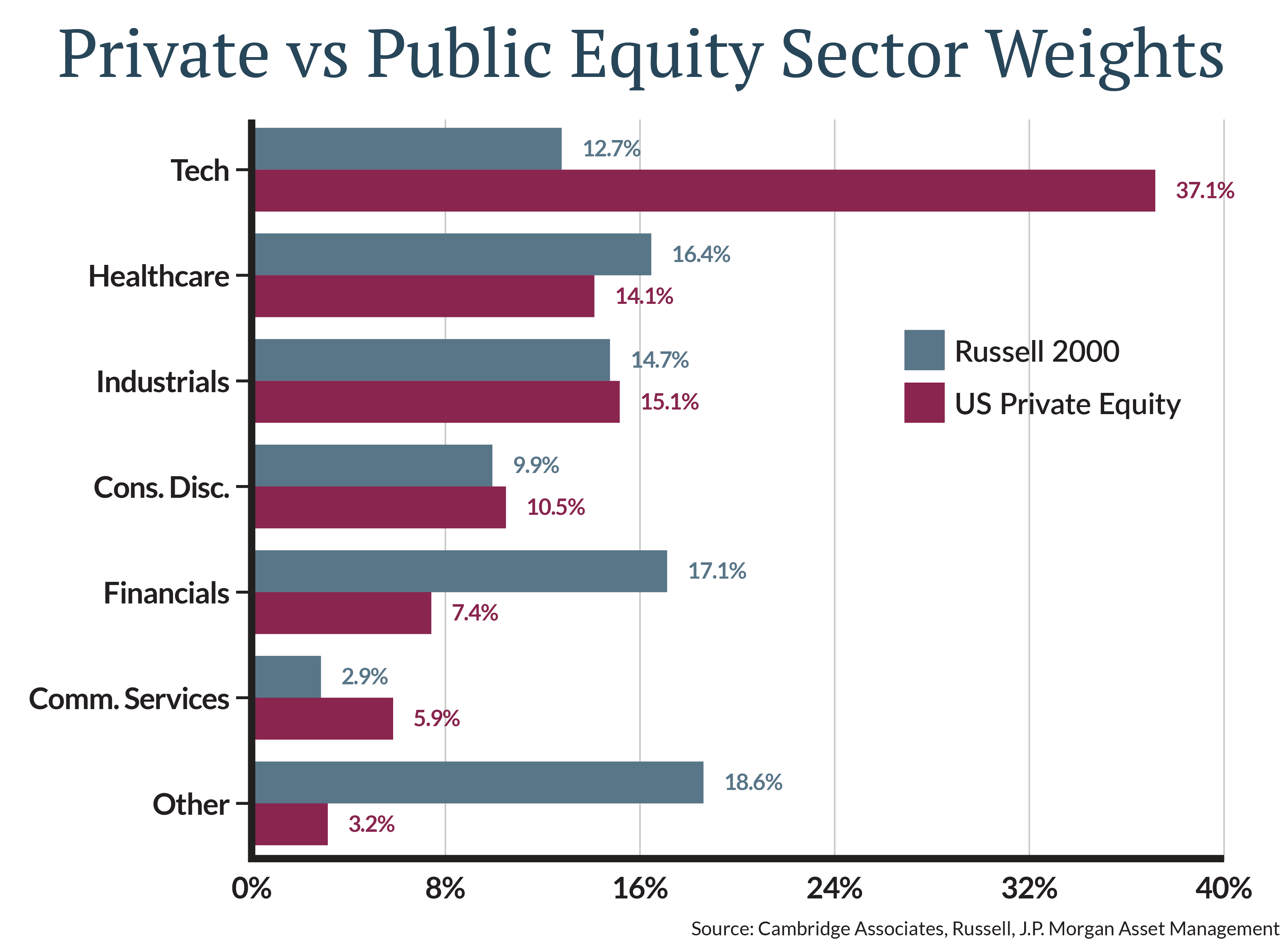

- ‘New economy’ businesses: As more businesses choose to remain private, a gap has emerged between the sector allocations of private equity-backed companies and the public markets, as shown below. [Figure 4] A significantly larger portion of private equity-owned companies are in the technology sector, an area of our economy with rapidly growing influence.

In summary, if current trends continue, investors who opt not to invest in private markets may be limited to a smaller pool of the economy that has fewer cutting-edge businesses and a larger share of unprofitable long-shots.

Change with the Times

We live in a fast-paced world where our attention is constantly being summoned by a new flashy object. Similar to my awakening to the growth of my daughters, many financial market observers are likely unaware of the magnitude of the change that has occurred from the persistent small shifts in the private equity world. In both cases, there's no turning back.

But, recognizing the current state and choosing what to do with that information is critical. Whether embracing private market investing is the right fit is an important conversation to consider with your advisor.

In my case, I'll be doing my best to embrace my daughters' childhood years as much as possible, and appreciating each stage as they grow. Undoubtedly, there will be some challenges and bumps along with the way, but I’m certain the best is yet to come.